Counterpoint Research

info@counterpointresearch.com

FOR IMMEDIATE RELEASE: 04/02/2025

Display Capex Forecast Raised on OLED Demand

Seoul, Beijing, Buenos Aires, Hong Kong, London, New Delhi, San Diego, Taipei, Tokyo -

- Display equipment spending forecast 2020-2027 raised by 2% to $77 billion.

- OLED penetration continues to increase in smartphones, tablets and laptops, but demand for IT OLED is lower than expected.

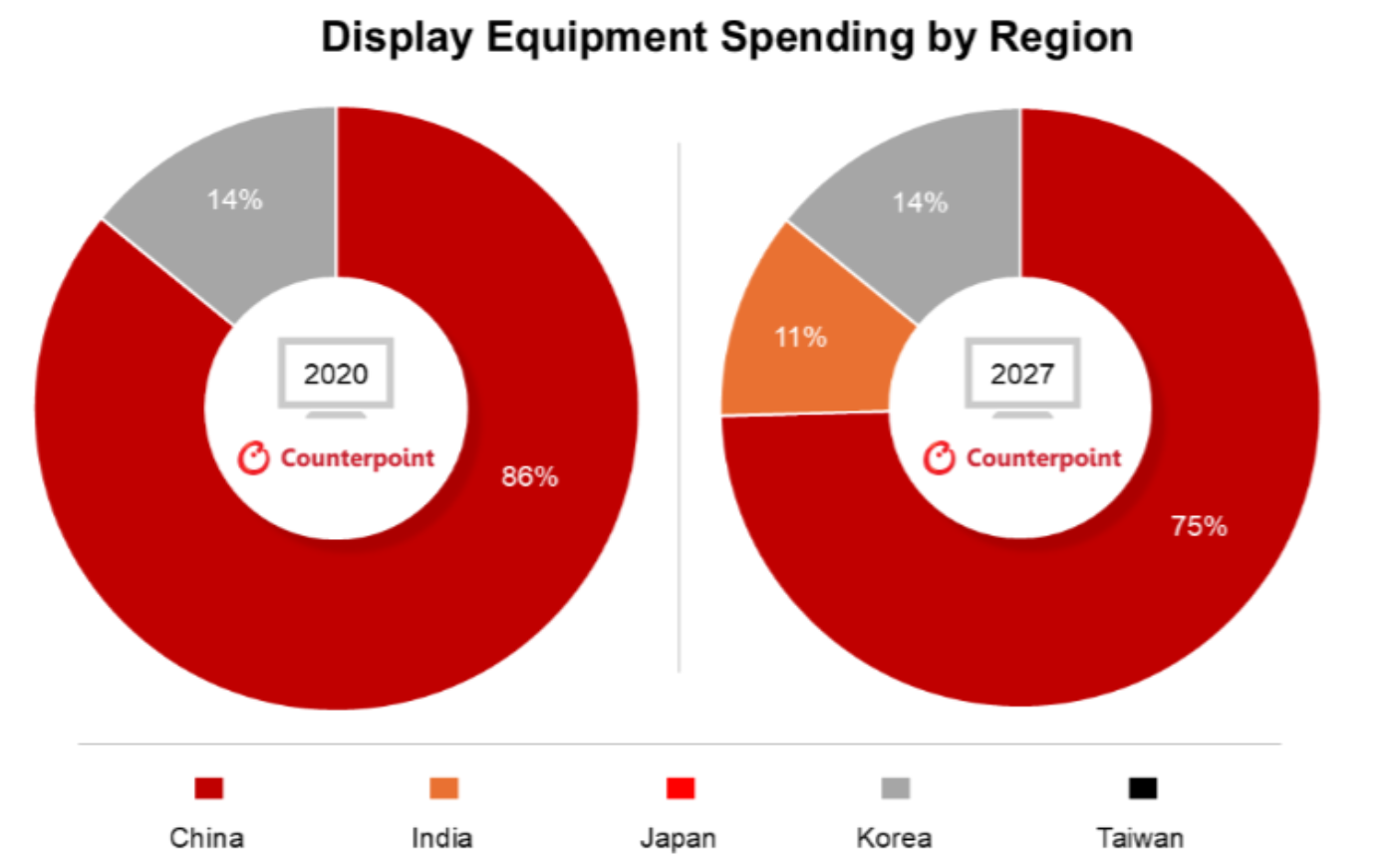

- China’s share of the 2020-2027 spending is projected to be 83%, with the country leading every year.

Seoul, Beijing, Buenos Aires, Hong Kong, London, New Delhi, San Diego, Taipei, Tokyo – April 2, 2025

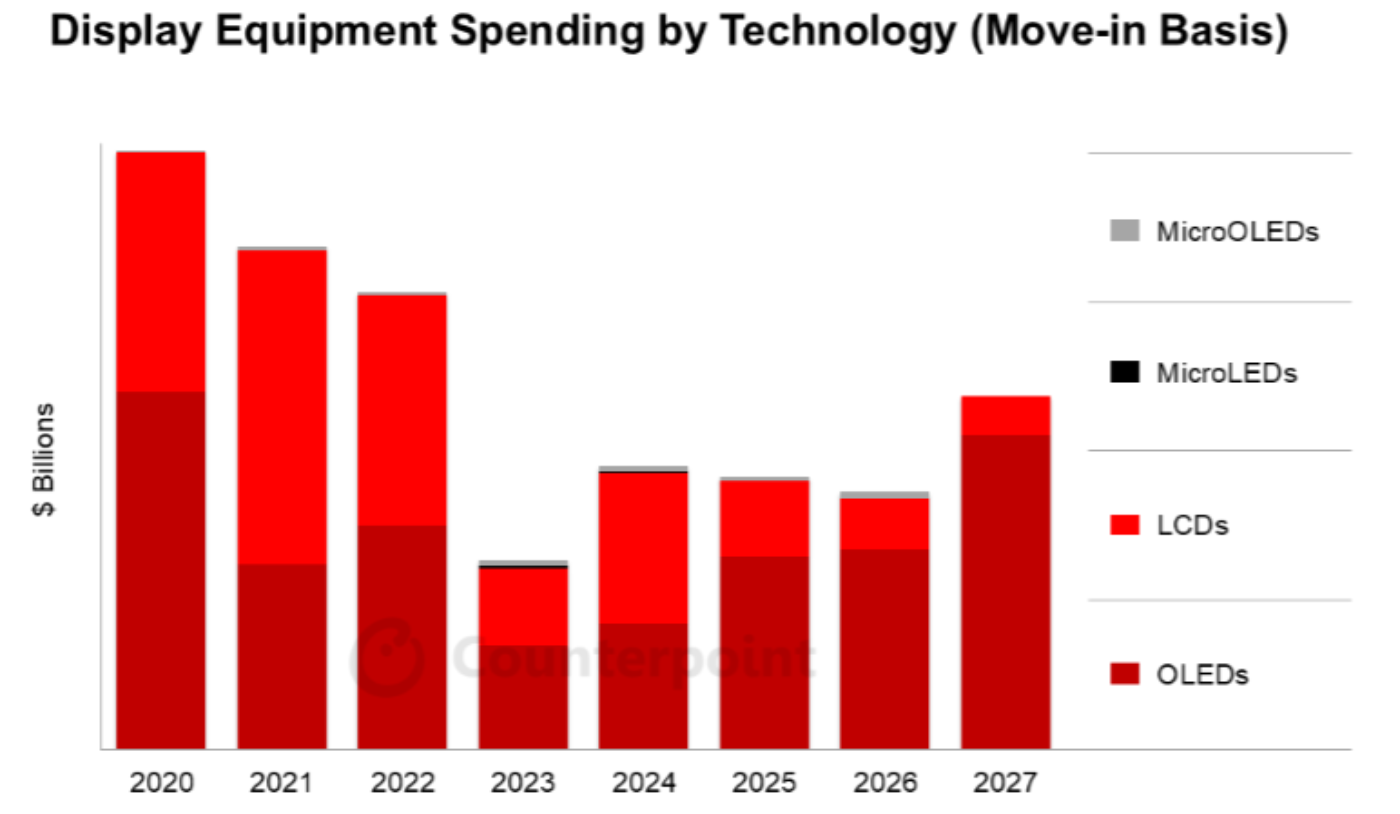

Counterpoint has raised its display equipment spending forecast for 2020-2027 by 2% to $77 billion on increased OLED spending and a slight bump in LCDs, according to its latest Quarterly Display Capex and Equipment Market Share Report.

The OLED increase can primarily be attributed to the flexible conversion of two G6 mobile lines and an additional 7.5K expansion at a G8.7 IT OLED line. OLED equipment spending is expected to increase each year from 2023 to 2027 to reach $8.3 billion in 2027 due to the addition of the G8.7 OLED fab, flexible/LTPO conversion and expansion in the >85” TV category. These in turn will be driven by rising OLED penetration across smartphones, tablets and laptops, and growing average panel sizes.

However, since the demand for IT OLED is not as high as expected, there is a possibility that smartphones will be produced first at certain G8.7 lines. While OLEDs are expected to account for a 58% share of the 2020-2027 display equipment spending on rising demand and higher capital intensity than LCDs, LCD fabs are expected to account for a 40% share with the conversion of large-sized >85” TV LCD fabs currently forecasted to be equipped during 2024-2027.

In terms of regions, China’s share of the 2020-2027 spending is projected to be 83%, down from 84% on $64 billion spent in Q4 2024, with the country leading every year. South Korea’s share of spending over this period is expected to be 13%, same as in the last quarter, on $10 billion spent. India is expected to account for a 2% share and Taiwan 1%. China is also expected to dominate LCD spending over the same period with a 93% share, OLED spending with a 77% share and Micro-OLED spending with an 85% share.

Equipment revenues are tracked for over 70 different display equipment segments with market share provided for each one. Over 170 different equipment suppliers are identified with design wins by segment.

About Counterpoint

Counterpoint Research acquired DSCC (Display Supply Chain Consultants) in 2023, joining forces to become the premier source of display industry research globally. The partnership combines Counterpoint’s thought leadership and expertise across the broader tech sector and DSCC’s deep specialization in display technologies to provide an unparalleled resource for insights and analysis for our clients.